A dramatic shift has been observed of late in the dynamics of the automotive sector, pertaining to which plating on plastics (POP) market has been undergoing a massive transformation of sorts. ‘Plating on plastics’ is basically a term that entails the application of metal on plastic substrates by means of electroplating for a decorative finish. As per the latest Plating on Plastics industry trends, automakers and OEMs have been striving to enhance the external appearance and the aesthetics of vehicles and making the surface highly resistant to wear & tear and corrosion.

Surveys depict that even consumers have changed their preferences toward automobile purchase and opt for buying vehicles endowed with high grade resistance and endurance properties. In addition, the appearance and the external look of the vehicle stands at the top of the priority list for customers. This factor is deemed to be a major driver for plating on plastics (POP) market size, which is predicted to surpass USD 649 million by 2023, with a target volume of more than 135 million square meters.

Plastic plating has been around since many decades – the operation was first commercialized in the 1960s in Europe and North America. Surface treatment was carried out using a chromic acid-based etchant on acrylonitrile-butadiene-styrene – a thermoplastic polymer more commonly known as ABS. The plastic’s adhesive properties were improvised with the help of this process, thereby establishing a strong bond between metal coatings and plastic substrates, and subsequently contributing toward the expansion of global Plating on Plastics industry. ABS then went forth to become the most popular and widely used polymer in plating on plastics industry. Even today, despite the availability of alternative polymers such as Teflon, polyetherimide, mineral-reinforced nylon, diallyl phthalate, urea formaldehyde, polycarbonate, polyacetal, and many others, ABS is still used in more than 90% of plating applications, significantly fueling global plating on plastics industry growth. Acrylonitrile butadiene styrene (ABS) market size, slated to grow at a rate of 6% over 2016-2024, is also projected to positively impact the business landscape.

Plating on plastics market: Debuting in the automobile sector

The 1970s first witnessed the usage of plastic plating on vehicles. Renowned automakers had then begun to develop manufacturing procedures to improve fuel economy, pertaining to the soaring fuel prices at the time. They discovered that manufacturing auto parts such as emblems, light bezels, and grilles with light, metal-coated plastic materials help reduce the total weight of the automobile, which subsequently leads to improved gas mileage. That’s how the concept of plating plastics and using them in the development of auto parts was introduced to commercialization, crediting the automotive sector with the tag of having contributed toward the expansion of Plating on Plastics industry.

The requirement for lightweight vehicles has grown considerably over the last few years. In addition, the demand for high performance polymers that provide increased automobile efficiency has also reached an all-time high, which will drive plating on plastic market size over the next few years. This growth can be primarily credited to that fact that high performance polymers used in the plating process impart steel-like strength to the vehicle in addition to offering flexibility in terms of vehicle design, shape, and size. Furthermore, the plating process helps reduce the vehicle weight and eliminate pollutions, which will propel plating on plastics industry growth.

Plating on Plastics industry: Depicting growth prospects due to changing trends in the automotive sector

The automotive sector is witnessing a plethora of trends subject to the increasing consumer demand for enhanced, high performance, and aesthetic looking vehicles. Lightweight vehicles depict a tendency to reduce carbon footprints, pertaining to which weight reduction in cars is viewed as a major feature that will impact its sales. In addition, stringent regulations enforced by organizations such as REACH to eliminate carbon and GHG emissions for safeguarding the environment has also led to reduced weight being a priority in vehicles, a factor which is expected to positively impact Plating on Plastics industry in the future.

A study depicted that lowering automobile weight by around 450 kg will lead to an approximate weight reduction of 40g of carbon dioxide. In addition, the fuel efficiency is projected to increase by a minimum of 8% and a maximum of 12%. This can be achieved by efficiently plating plastics for auto parts. Currently, polymers account for almost 15% to 20% of the vehicle weight, including the exterior & interior components. Their increased usage in the plating process will eventually lead to substantial growth of plating on plastics industry.

The plating process helps increase the corrosion resistance of the vehicle surface, increases the strength of the vehicle, and protects it from wear and tear. It also enhances the appearance of the vehicle, provides a shiny, glossy finish, and lends the impression of a high quality, expensive purchase, which will significantly augment plating on plastic market size.

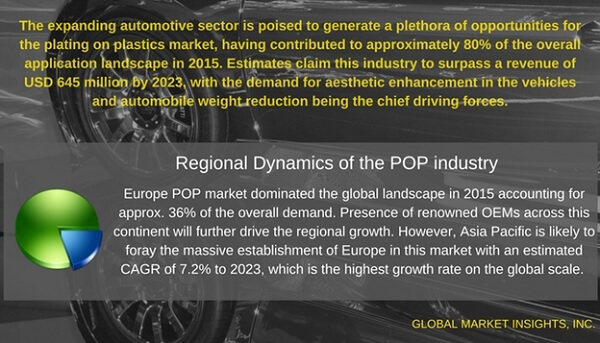

Automotive applications led the overall plating on plastics industry by accounting for more than 79.9% in 2015, with a revenue collection of USD 295 million. The high requirement for lightweight and fuel-efficient vehicles coupled with the introduction of varied, high grade automobile models every year will propel the growth of Plating on Plastics industry.

Plating on plastics industry polymers such as ABS, PEI, PC, PEEK, PC/ABS, PBT, PET, and LCP are currently used to plate numerous components of automobiles, such as license plate frames, mirror housings, reflective surfaces, radiator grills, interior & exterior trims, gear knobs, wheel covers, door handles, light bezels, and logos & emblems. This has provided lucrative opportunities for OEMs to come up with high grade automobiles. Even the automotive aftermarket, renowned for manufacturing spare parts, has been predicted to gain lucrative revenue from the growth of plating on plastics market.

Plating on plastics industry growth potential across the Asia Pacific belt

The automotive sector has been experiencing a rather lucrative growth rate across the Asia Pacific over the last few years. This is essentially due to increased automobile demand across the emerging economies such as India and China, rising deployment of advanced technologies in cars, increasing disposable incomes, and changing consumer lifestyles.

The total automobile production in the Asia Pacific region was 47.60 million units in 2014. This number increased to 47.99 million units in just a year. Automakers such as Nissan, Suzuki, Honda, Toyota, and Mitsubishi and auto parts manufacturers have been shifting their production facilities in APAC owing to favorable government support in the form of tax rebates and other incentives, which will consequently lead to the growth of plating on plastics market. Countries such as Malaysia, Thailand, and Indonesia are also expected to join the elite list of major revenue contributors toward APAC Plating on Plastics industry.

China lead the APAC plating on plastics industry in 2015, and is expected to observe a CAGR of 7.2% over 2016-2023. Driven by China, Asia Pacific Plating on Plastics industry is forecast to witness the highest gains over the next six years. China plating on plastics industry size from automotive applications is expected to cross a revenue of USD 115 million by 2023, with a CAGR estimation of 7.9% over 2016-2023. This growth can be credited to the shifting of OEMs in the region coupled with the extensive increase of automobile sales in the nation.

Automakers depend heavily on POP industry players to adhere to the strict guidelines laid down by regulatory bodies. While a strict regulatory framework designed by organizations such as OSHA, REACH, and EPA has helped enhance Plating on Plastics industry share, it can also pose a threat to its growth over the next few years. This is essentially due to the fact that chrome plating can lead to severe health hazards. In addition, excessive chrome plating has been found to cause environmental damage. To combat this restraint of Plating on Plastics industry, leading companies are coming up with alternative means, such as nickel and copper plating.

Reportedly, REACH has formulated norms in the European Union (EU) for OEMs to eliminate the usage of chrome constituents completely in their vehicles. The deadline for the same is the 21st of September 2017. Plating on plastics market participants such as Dow Electronic Chemicals, Enthone, and Oerlikon Balzers have already begun to develop innovative products that exclude chromium trioxide and yet lend the same aesthetic, glossy appearance to automobiles. Similar efforts by other industry players are further expected to fuel global plating on plastics market over the years to come.

Global Market Insights, Inc. has a report titled “Plating on Plastics (POP) Market Size By Finish (Chrome [Cu, Ni & Cr]), By Plastic (ABS, PC, PC/ABS, PEI, PET, PBT, LCP, PEEK, PP, Nylon), By Application (Automotive, Domestic Fittings, Electronics & Electrical), Industry Analysis Report, Regional Outlook (U.S., Germany, UK, China, India, Brazil, Saudi Arabia), Application Potential, Price Trends, Competitive Market Share & Forecast, 2016– 2023” available at https://www.gminsights.com/industry-analysis/plating-on-plastics-POP-market .